Insights and Strategies

Winter Is Coming

It was House Stark of Winterfell that ruled the North from their fortress in Winterfell, in the hit fantasy TV series Game of Thrones. Ned Stark, also known as the Lord of Winterfell and Warden of the North, popularized the term “winter is coming”, which became a common phrase used throughout the series to suggest that tougher times were ahead. While we too expect the upcoming winter to be a harsh one here in the North, in a similar vein, we believe investors should be prepared for a more challenging, volatile, and unpredictable economic and market climate heading into 2023.

Moreover, as we discussed in detail in our latest Quarterly Asset Allocation report: Stop! Hammer Time, we continue to anticipate the level of uncertainty to remain elevated as central banks continue to tighten policy despite the growing risks of a hardlanding/ recession on the horizon. Canada’s inflation rate continues to run hot and remains elevated with the latest reading of the Consumer Price Index (CPI) for June rising +8.1% year-over-year (YoY). We expect CPI readings for the remainder of the year to hover around +7% which is ~2-3x above the neutral range of ~2% that the Bank of Canada (BoC) has historically targeted - the level of inflation which is neither expansionary nor restrictive for the economy. But with the level of inflation well above this target range and labour markets still extremely tight, aggressive policy tightening efforts are currently the only tool the BoC can use to help bring down inflation towards more reasonable levels.

However, we remind investors that changes in monetary policy (i.e., rate increases/decreases) not only have a delayed impact on the real economy, but they also do very little to help alleviate temporary and/or structural inflationary impulses associated with China lockdowns, Saudi/Texas drilling, quarantines, refining capacity, war, supply-chain on shoring, etc. We expect this aggressive pace of tightening to weigh heavily on domestic demand, with measures of spending growth falling sharply including with residential investment, which we believe will fall back to pre-pandemic levels.

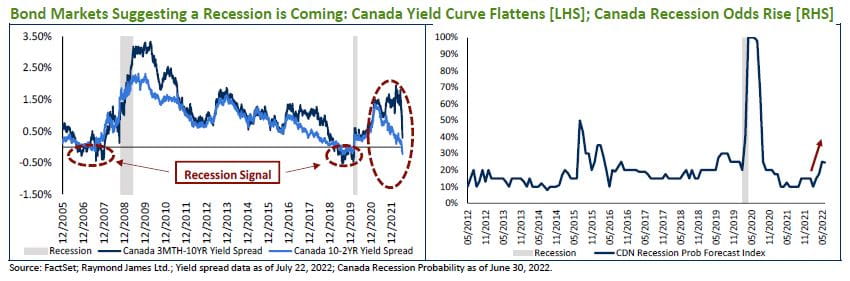

The bond market, which historically has been a fairly accurate predictor of recessions, is currently signaling a higher risk of a recession for the Canadian economy over the next 12 months. We see the odds of a recession increasing from here, especially if the BoC continues to tighten monetary policy aggressively into year-end.

![Bond Markets Suggesting a Recession is Coming: Canada Yield Curve Flattens [LHS]; Canada Recession Odds Rise [RHS]](/-/media/rj/dotcom-canada/images/commentary-and-insights/markets-and-investing/insights-and-strategies-aug-2022.jpg?h=281&w=850&hash=080E06C212732D0DD5E189B7FAEAC137)

{kind=link}